China’s Government Guidance Funds 💰💰💰

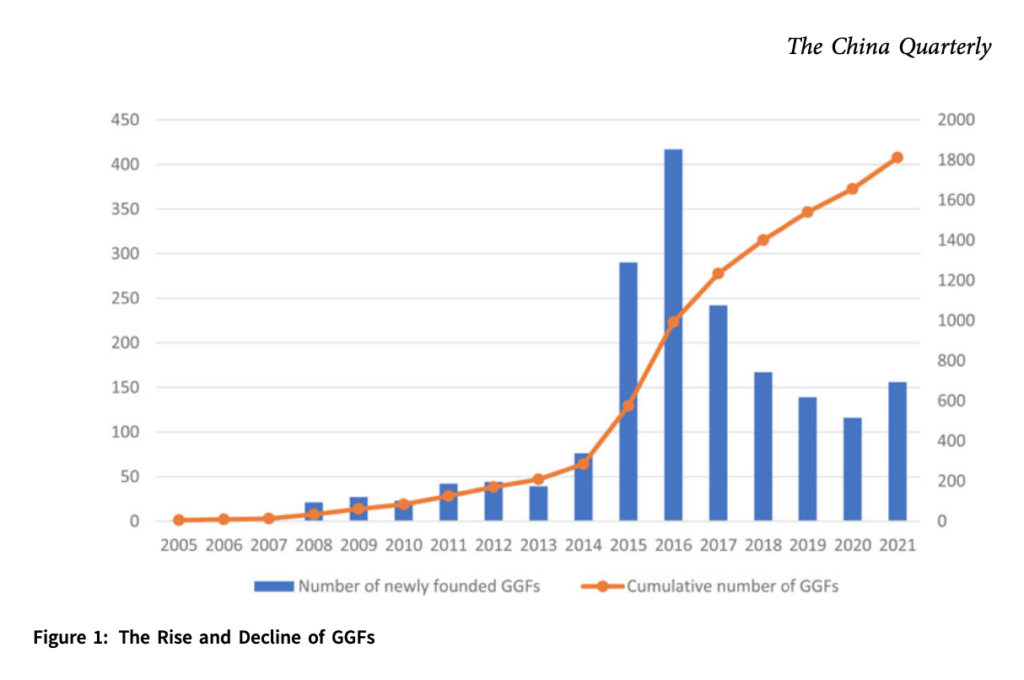

Did you know that China has more than 1,800 so-called “government guidance funds” (GGFs, 政府引导基金), partly state-managed VC firms with a target capital size of 11 trillion RMB (1.55 trillion USD) supposed to provide patient capital for investments into crucial infrastructure and deep tech?

In 2005, the Chinese government deployed GGFs as a new financial instrument to accelerate technological catch-up. GGFs are funds established by central and local governments partnering with private venture capital to invest in state-selected priority sectors.

Although, according to Zero2IPO, a Chinese independent market research firm of venture capital (VC) and private equity (PE) investment in China, GGFs had raised only 4.76 trillion CNY / $672 billion (= 43% of their targeted volume) in the first quarter of 2020 and still fall back behind their initial targets in 2023 (no current statistics found), they DO effectively support deep tech and startup growth in China:

A subset of disciplined, market-oriented guidance funds, foremost in Shanghai, Beijing & Shenzhen, is successfully raising money and investing in projects (incl. deep tech), the reason being that Shanghai, Beijing and Shenzhen are exceptionally capable of attracting and retaining high potential ventures.

Looking at funding rounds, GGFs are often among the investors and co-finance as many as 1/4 to 1/2 of all Chinese financing rounds. As GGFs are closely aligned with the Chinese 5-yrs plan and the local governments’ economic growth targets, they can dynamically shift their focus to supporting tech verticals which are Chinese national top priority at a given time.

KEY FACTS:

- Target capital ratio (state/private):

20-30% state budget / 70-80% private funding.

In practice, though, many LPs in guidance funds are state-funded entities, such as state-owned enterprises (SOEs) and state-run banks. - Target sizes national vs. provincial level:

Local & provincial funds: < 10 billion CNY (< $1.4 billion).

National-level funds: > 10 billion CNY (> $1.4 billion). - Distribution across China:

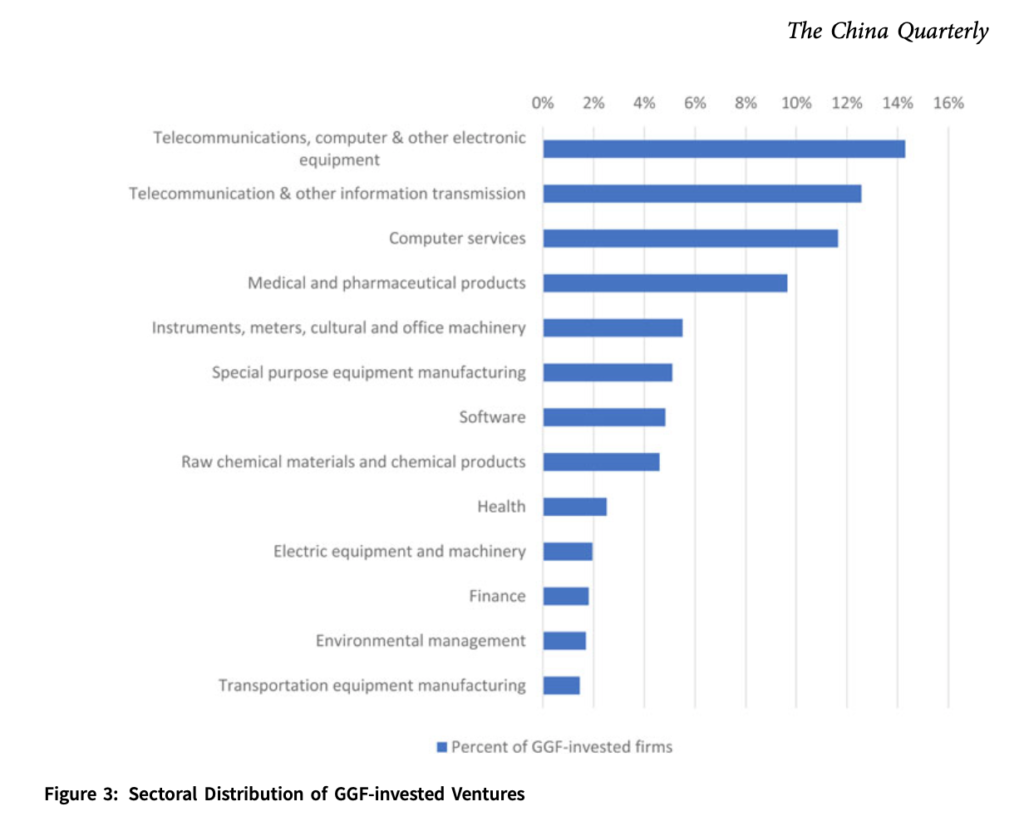

Most active GGFs are located in TIER 1 hubs #Beijing, #Shanghai, and #Shenzhen. These are also the ones using their funds to invest in #deeptech #startups (while most others tend to invest more in SMEs, soft tech and crucial infrastructure).

STRUCTURE:

- The fund itself is an entity formed by or at the behest of a central, provincial, or local government agency.

- Typically, the governmental sponsor creates the fund, sets a fundraising target, allocates capital to part of that target directly from budget outlays, and tries to raise the rest from other investors, whose contributions are called “social capital” [社会资本].

- GGFs usually use the LP structure common in equity finance worldwide.

- A guidance fund’s GP may be …

a) a fund management institution established by a government agency,

b) a state-owned investment company, or

c) a third-party professional fund manager.

INVESTMENT STRATEGIES:

Guidance funds use different investment strategies:

- Some invest directly in companies or tangible projects, such as factories and industrial parks.

- Others employ a fund-of-funds approach: they invest in other investment funds (including other guidance funds), and these “sub-funds,” in turn, invest in actual projects and businesses.

ECONOMIC EFFECTS:

The effects on fixed assets and employment are significant. Firms that received investment from the fund increased their fixed assets by approximately 50 percentage points and their employment by 20 percentage points above average levels.

WEAKNESSES TO OVERCOME:

- Guidance funds often raise much less money than planned.

- Much of the money guidance funds raise is never actually invested in projects

(partly because of poor management, partly due to the lack of quality ventures, which is particularly acute in provinces with weak entrepreneurial bases and high-tech industries). - There are too many guidance funds leading to redundancy and inefficiency.

- Many guidance funds are poorly managed.

- Many guidance funds do not invest in early-stage companies as intended.

More about the performance of GGFs in:

Yifan Wei, Yuen Yuen Ang and Nan Jia:

“The Promise and Pitfalls of Government Guidance Funds in China”

(The China Quarterly / Cambridge University Press)

“In practice, however, there are notable gaps between policy ambition and out-comes. Our analysis finds that realized capital fell significantly short of targets, particularly in non-coastal regions, and only 26 per cent of GGFs had met their target capital size by 2021. Several factors account for this policy implementation gap: the lack of quality private-sector partners and ventures, leadership turn- over and the inherent difficulties in evaluating the performance of GGFs.”

Further reasons for poor performance include:

- Lack of quality partners:

One reason behind the shortfall in fundraising is that it has become increasingly difficult for GGFs to attract quality VC/PE partners to help raise private capital. According to the National Audit Bureau (NAB), in 2016 private capital accounted for only 15 per cent of the capital raised among a sample of 235 GGFs in 16 provinces.

Leading VCs/PEs are less likely to participate in GGFs since they have plenty of opportunities to raise capital from the market and do not need government seed funds. Government funds are not small in absolute numbers, but are relatively insignificant compared to the capital pool managed by leading VCs/PEs. For example, Matrix Partners China (Jingwei Zhongguo 经纬中国) has a capital pool of over 50 billion yuan, compared to the million-dollar seed funds that most GGFs offer.

In contrast, lower-tier VCs/PEs, which need government funding, are more willing to participate in GGFs. But such companies are less able to attract additional capital from the market to meet financing targets. - Leadership turnover:

Local leaders in China have relatively short time horizons. Most are rotated after only a few years in office. After incumbent leaders leave office, their GGFs are usually left unattended, similar to white elephant construction projects. Successors do not want to be responsible for their predecessors’ GGFs and simply create new GGFs to showcase their own performance.

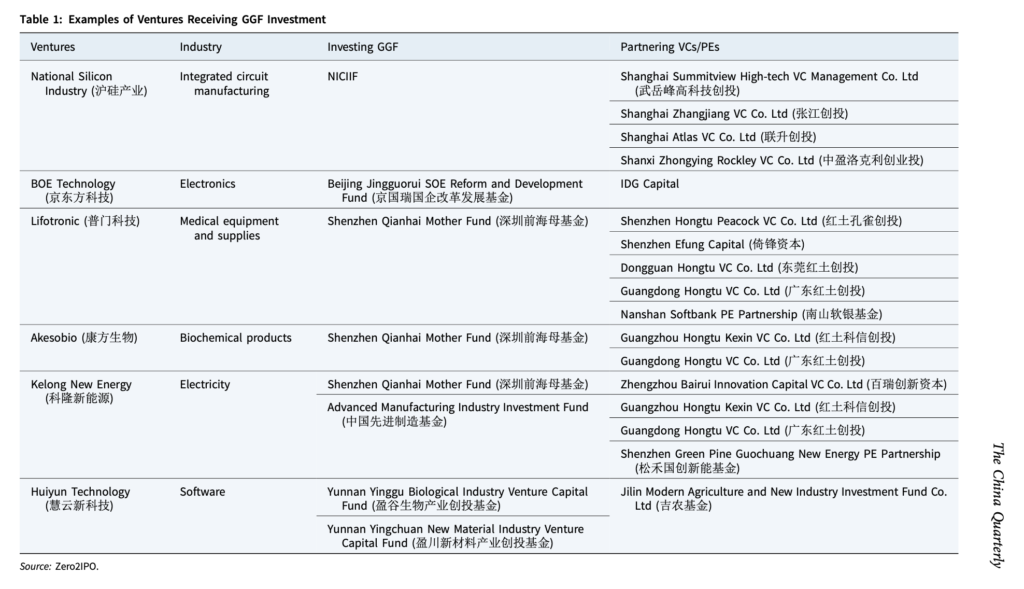

SELECTED TABLES AND GRAPHS:

CREDIT:

https://cset.georgetown.edu/publication/understanding-chinese-government-guidance-funds/