By ChineseAlpha & NIUCAP VENTURES, July 10, 2022,

Authors: Niklas K. Bruns, Bettina B. Scheibe, Xinqi Wang

Key Points

- Rising wages and geopolitical tensions เกม pg drive divestment trends of foreign companies in China.

- The future of China’s manufacturing industry lies in the development of high-tech manufacturing.

- China is expected to retain its position as the leading manufacturer despite toughening competition from other developing countries in South East Asia.

Introduction

If you check the tag of any number of products, chances are high you’ll find the words “Made in China”. During the last decade, it seemed like everything has been made in China including iPhones, Nike shoes, Barbie dolls, Levis jeans, Dell computers and much more!

In 1949 the People’s Republic of China was formed under the leadership of Chairman Mao Zedong, accompanied by economic reforms, limited regulations, low wages, a massive workforce and strategic trade relationships. This combination of factors led China to unprecedented growth and ultimately, through the economic reforms by former president Deng Xiaoping in the late 1970s, became the “Factory of the World”. In 2010, China achieved to grow into the world’s second-largest economy and its economy is consistently expanding at about three times the pace of that of the United States. China is currently the world’s largest exporter by value with about US$3.026 trillion worth of products being sent around the globe [1].

Despite China’s impressive history in manufacturing, there are signs that this trend may not be continuing as strongly in the years to come. Due to soaring labor wages in China and political tensions, for a couple of years now, international organizations are increasingly diversifying their supply chains to other South Asian countries such as Vietnam, Bangladesh, Thailand, Sri Lanka, Cambodia and India.

Exodus of Manufacturing from China

But how did this happen? — The price and speed at which China was able to produce goods started to slow down as the country’s population grew and its presence on a global stage drew attention to environmental and wage regulations.

Specialisation started driving labor costs up, resulting in the average manufacturing labor rates paid to Chinese workers climbing to about US$150/year in the 1990s, and settling at around US$14000/year. Today, workers in other developing countries, such as Sri Lanka, undercut Chinese workers with their meager wages of around US$2000/year. As a result, manufacturing of products with low margins and simple production processes, like textiles, shoes and electronics, has started drifting to other countries years ago [2].

The state of manufacturing in China is coming close to a tipping point and the country is forced to increasingly automise its manufacturing landscape while building a more service-based economy with an enlarging focus on e-commerce and technology.

Apart from rising wages, geopolitical tensions are another factor driving divestment trends of foreign companies in China. Particularly Japan’s leadership has grown concerned about its dependence on China in the future and as a result of increased pressure, Samsung closed its last smartphone, computer and TV factories in China in 2019 and moved production lines to Vietnam.

Since 2020, the Japanese government has been compensating Japanese companies that decided to divest in China with special subsidies, and as a result, Olympus, Mitsubishi, Toshiba, Panasonic, Sony and Nikon soon followed suit with Samsung.

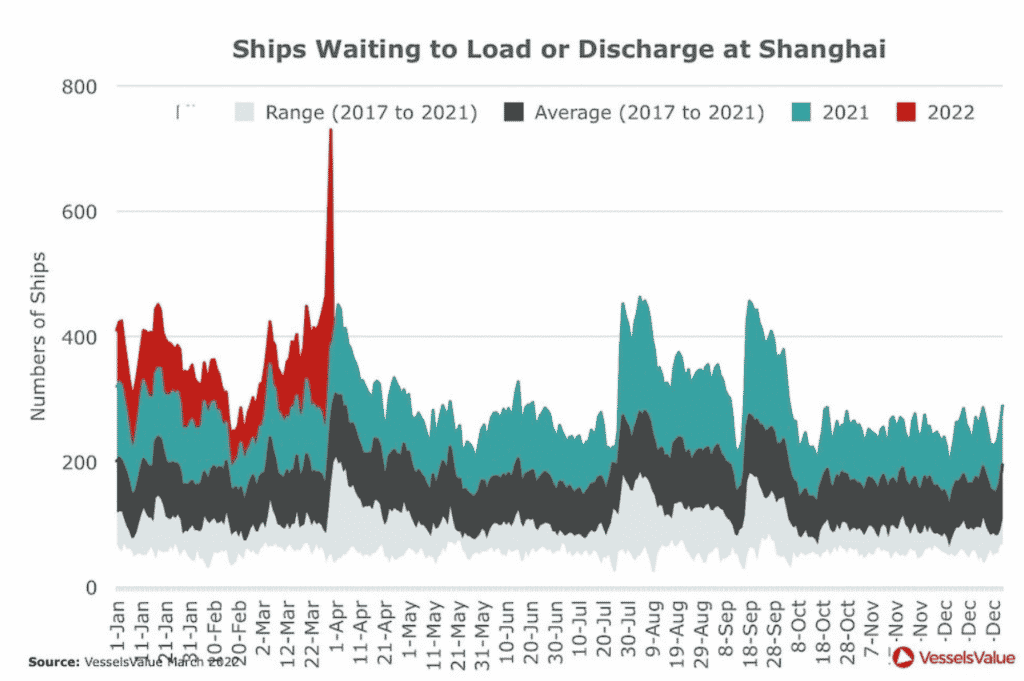

These trends have been further fuelled by the pandemic and the frequent lockdown situations in various major Chinese cities, including the vital port city Shanghai. Across China, about one quarter of the country’s population (373 million people) have been in Covid-related lockdowns in the first two quarters of 2022. The heavy operational difficulties in the prolonged outbreaks of COVID-19 have led world-renowned optical and industrial products manufacturer Canon to shut down its China factory after 32 years of operations, despite a preceding major 1.5 billion Yuan investment in 2013 into China. The difficulties and pressure to stabilise growth within the Chinese economy have been unprecedented in the last 3 pandemic years and many Chinese companies have been working under significant supply and production instabilities. Many Chinese supply chains have been cut off as a result of unreliable delivery of parts and components.

European multinationals have experienced especially tricky value chain challenges due to Chinese supply chain disruptions and if there is no increased stability guarantee going forward, an increasing number of European companies will be inclined to switch to near-sourcing models in the future. In addition, the efforts of other developing countries to take back overseas industries, as well as the effects of rising material prices are putting serious pressure on Chinese manufacturing. China’s exports increased only by 3.9% in April 2022 year to year, the weakest rate since a 0.18% gain in June 2020. Exports in Vietnam, on the other hand, increased by 30.4% in April 2022 year to year [3].

The manufacturing exodus can be especially seen in the apparel and footwear industry. Prior to 2010, China was the largest manufacturer of Nike footwear. Today over half of all Nike shoes are being produced in Vietnam. This year, Vietnam has taken China’s spot as the largest producer of ADIDAS shoes with 42% of all shoes produced in Vietnam and only 15% being produced in China [4]. Japanese fashion brand UNIQLO had produced just shy of 90% of all products in China back in 2013 and today only produces roughly 50% of its items in China [5]. The rapid decrease in China’s apparel manufacturing dominance shows the pace that other countries can replace China as the leading manufacturer.

So, while companies operating in any part of the world are confronted with increasing economic risks and uncertainties caused by geopolitical developments, increasing raw material costs, growing labor costs and the shortage of critical materials, investors particularly start to question how dependent one should be on the Middle Kingdom. The pressure imposed on stock-listed international companies by their investors forces C-level executives into rethinking their risk diversification strategies and, above all, their future investment plans. As a result, many foreign corporations have put new investments in their infrastructure in China on hold.

China Bears the Fruits of a First-Mover Advantage

Does this mean China’s manufacturing industry is about to be completely replaced? — Not quite!

China will still remain the world’s manufacturing giant if the country seizes its chances of growing and enhancing its high-tech manufacturing. Most of the parts that are moving away have comparatively small margins and simple production processes; it is typically the basic outsourcing that is being relocated. Today China still has a considerable advantage vis-a-vis upcoming manufacturing locations. Capital is still invested in China’s manufacturing industry and factors such as in-place infrastructure, long-term supplier relationships and access to talent give Chinese manufacturing an unfair advantage.

Withdrawal of labor-intensive manufacturing, such as footwear and apparel, has been especially noticeable as labor costs and trade tariffs in China have been on the rise, making other south Asian countries a better place to manufacture products, but nevertheless, extreme decoupling cannot be expected. One has to look at which parts of manufacturing are moving away and which parts aren’t. There are some parts that are moving away like textile and shoes, but it remains China’s priority to be “The Electronics Factory of the World” in the future.

China’s Ministry of Commerce states that foreign direct investment into the country increased by 26.1% year on year to $74.47 billion for the first four months of 2022. During that period, German investment in Germany increased by 80.4%, whereas American investment in the US increased by 53.2%. Thus, the future of manufacturing will be a diversified landscape, and China won’t be the only manufacturing center in the world.

Manufacturing Investments Become More Focused

The future of China’s manufacturing industry lies in the development of high-tech manufacturing, of which the support of national policies is an effective promoter. Because Beijing has pushed hard to apply AI across China’s economy and society, “AI governance” and “ethical AI” have become buzzwords that frequently appear in government policy papers and corporate documents, according to Sheehan, a fellow at the Carnegie Endowment for International Peace who studies global technology issues with a focus on China.

The Metaverse, a popular topic especially when it comes to discussing how technology has the potential to change the way we work, live, and play will ignite the manufacturing revolution in China. Manufacturers contribute specialised knowledge and a thorough understanding of many of the critical technological enablers required to bringing the Metaverse to life. By exploiting the current manufacturing trends, such as flexible hybrid circuits, miniaturization, microfluidics, sensor technologies, AR/VR, and digital twins, to mention a few, we are likely to have 85% of the jigsaw pieces needed to build the Metaverse [6].

In addition, the Industrial Metaverse powered by simulations, which allows organisations to test the impact of potential decisions on their systems, machines, factories and business operations and understand future timelines, will help them better manage uncertainty about their existing capabilities, legacy product demand, and market and regulatory sentiment shifts [7]. They’ll figure out new methods to put the assets they’ve built up over decades to work for them, such as logistics and supply chains, as well as the ability to mass-produce millions of items on a worldwide scale. Most importantly, they will be able to select the most effective techniques for furthering their goals and change those strategies in real-time to accelerate and genuinely transform.

China is purchasing more robots each year than Japan [8] and while China has not yet caught up to the United States in terms of domestic manufacturing, this is changing, as is the kind of robots it creates. Some industrial jobs that require a human touch have shifted to Southeast Asia due to growing labor costs in China. If China’s future of cost-effective production is transferred to mechanical hands, China’s industrial robot market’s strength and development potential in tandem with its push for innovation and R&D expenditure might give it an iron edge for years to come [9].

Apart from AI, software-centric techniques such as robotic process automation (RPA) are also gaining traction among investors [10]. Despite the fact that China’s RPA industry is still in its infancy compared to more established competitors, it is gaining traction as the country’s manufacturing robots environment expands. In the spring of 2019, benchmarking businesses in China quadrupled in three months, mirroring a significant surge in US valuations, with interest from Coatue Management, a technical hedge fund, and Masayoshi Son, the CEO of Softbank [11]. Nevertheless, sustainability of the smash-and-grab attitude advocated by newcomers in the business is questionable.

China has been the biggest market for industrial robots since 2013, and already held share of 41% of the global industrial robots market in 2018. China’s share in the global robotics market has been growing by 10% in 2021, and is expected to continue to grow in the upcoming years. To further build out its future as a smart manufacturing hub, China aims at becoming more independent of global suppliers. This is why the country has been investing heavily in its own domestic robotics companies. While in the first ramp-up stage of China’s high-end manufacturing, the Middle Kingdom mainly installed robots of Japanese and German manufacturers, it’s aiming to double domestic companies’ market share from 30–40% to 70% by 2025, as stated in China’s former strategy paper “Made in China 2025” [12].

From an international standpoint, this would mean that global manufacturers will no longer sell big to Chinese factories, but will most likely be steadily pushed out of the market, while domestic manufacturers of robots will be seeing no limits.

Chinese VCs are Moving Into the Robotics and Industrial Space

Since domestic robotics, robotic process automation software (RPA) and industrial applications are now becoming a growing domestic industry sector, which is also being supported by the central government, this space is becoming more and more popular among Chinese VCs. Even VCs who have been formerly focused on fields such as e-commerce, internet technology and gaming, are now moving into the industrial space. Investments in corporate services, artificial intelligence (AI) and industrial internet of things (IIoT) solutions are also gaining traction.

To increase the momentum of this trend and further boost investments in B2B, a new form of funding vehicle has been installed by local governments: In the first quarter of 2020, Chinese officials set up 1,741 so-called “government guidance funds”, with a registered target size of 11 trillion RMB (1.55 trillion USD).

Government guidance funds have a dual mandate to produce financial returns and further the state’s industrial policy goals. As an industrial policy tool, guidance funds have several potential advantages [13]:

- Guidance funds allow the Chinese state to leverage market discipline and expertise.

- Guidance funds offer patient capital, a critical resource for emerging technologies.

- Guidance funds can complement and amplify other industrial policy measures, producing robust, holistic support for emerging and high-tech businesses.

In practice, most guidance funds still fail to live up to their ambitions, it’s still a clear signal of the direction China’s taking. It also makes clear how much the Middle Kingdom is willing to invest to strengthen its position as “The World’s Factory” by becoming “The World’s Smart Factory”.

As for classical VC, the race for B2B talent is on and B2B investments are considered the “new gold rush frontier, fuelled by large sums now flowing into the sector.” While return & scaling expectations still need to be calibrated to the new industry (often very too high since experience has mainly been gained with hyper-scalers in e-commerce) and a deep understanding of the industrial space often still needs to be gained, Chinese VCs like Sequoia Capital China, Lightspeed China Partners, Hillhouse Capital Group, BlueRun Ventures, and Bertelsmann Asia Investments set high expectations on the same. Especially fields like the Industrial Metaverse, smart business solutions, robotic process automation (RPA) and robotics, where experience and know-how from e.g. e-commerce, internet technology and gaming can be transferred, are on the rise [14].

Conclusion

There are various scenarios where parts of manufacturing are moving to other markets and it is becoming more difficult to convince investors to envision China as the future of manufacturing for the next 5–10 years to come.

There are several reasons manufacturing is leaving China. The Chinese government’s unfair treatment of foreign enterprises and the inappropriate transfer of technology from foreign firms [15] paired with the gap in China’s import to export of merchandise gives foreign leadership reason to promote a manufacturing exodus from China. Besides that, the supply chain issue, soar in labor costs, and decrease in output resulting from the lockdowns also trigger divestments from China. It can be expected that China will face toughening competition in manufacturing from other developing countries in South East Asia [16].

Even with the many risks and uncertainties, it’s quite unlikely that China’s position as the world’s factory will be completely replaced in the future. China appears to be ready to face the challenges of the future head-on and adjust as necessary to maintain its status as an economic powerhouse. China’s capability of seizing the opportunity to develop high-tech manufacturing such as AI and robotics has the potential to upgrade its traditional manufacturing industry to the next level.

There are reasons for China to grow the advanced manufacturing industry. Automation goals are typically centered on driving up production volume and driving down labor costs. Automated lines were essentially “fixed,” with limited ability to modify once in place. In periods of stable demand, companies were willing to make these tradeoffs.

Today being a high-volume producer is no longer enough. Companies who embrace “software-defined automation” can more easily reprogram a line, adjust production output as market conditions shift, and even replicate operations from one factory to another. They can reduce the downtime and start-up costs that are often prohibitive when considering a capacity expansion. Advances in automation also make it possible to build multiple SKUs on a single line, employing software-based instruction sets that can be selected and run by line operators right on the factory floor.

However, investors interested in high-tech manufacturing (B2B) in China need to pay attention to the following dimensions: B2B requires a much more top-down approach and the leveraging of industry research. Foresight to identify high-quality projects early on, as well as higher requirements for industry awareness and the formulation of top-level investment strategies, which necessitates thinking from the macro dimension.

In the B2B world, financing cannot directly promote the development of businesses since B2B is not a capital-intensive sector. In comparison to B2C projects, investors in this industry should analyse funding more thoroughly and meticulously.

Authors & Sources

This article was published by NIUCAP VENTURES and Chinese Alpha, as was the respective podcast edition of China Tech Chat.

Authors:

- MA. Bettina B. Scheibe: MD of NIUCAP VENTURES

& CTC Podcast Co-Host — LinkedIn - MSc. Niklas Kimo Bruns: ChineseAlpha Senior Equity Analyst

& CTC Podcast Co-Host — LinkedIn - MSc. Xinqi Wang: ChineseAlpha Guest-Author — LinkedIn

Sources:

https://kr-asia.com/as-wages-in-china-climb-robots-are-making-everything-you-buy

GIZ (April 2021): China’s implementation of Industry 4.0 (in collab with Germany Trade & Invest)

Germany Trade & Invest (GTAI): Export industry in South China automates its manufacturing (German)

Mercator Institute for China Studies (MERICS), April 2020: New MERICS study on Made in China 2025

McKinsey (2021): The future of digital innovation in China

Protocol.com (end of 2021): Open source in the context of Industry 4.0

Protocol.com (May 3, 2022): What’s the next big milestone in factory automation?